Income Straits of RAAs

Income Straits of RAAs

+Income Buffers for RAAs

Income Straits of RAAs

A higher proportion (70%) of the retired, aged, and ageing population in Nigeria earn N50,000 per month or less or nothing, according to a study sample by Dataphyte and JAIRAA.

At this income level, the retired, aged, and ageing (RAAs) live below the global poverty line.

According to the World Bank, the poverty line is estimated at $2.15 or N3,190 per day (at N1,484 per dollar).

Given that a month has thirty days on average, the average monthly living cost at the poverty line amounts to N95,700.

This amount is N45,000 more than the income earned by most retirees in Nigeria

Source: Dataphyte research

The lack of social security, poor social services, and subpar medical facilities make Nigeria's elderly vulnerable to disease and poverty, according to an African Health Sciences Journal.

While some older individuals struggle to make ends meet and depend on friends, family, and children for support, others resort to begging as a means of livelihood.

Reducing poverty in the elderly needs full participation from other age groups. This means that to avoid and end elder poverty, other age groups must work towards it either by saving to prevent them from suffering the same fate or by providing financial support to retirees.

Income Options for RAAs

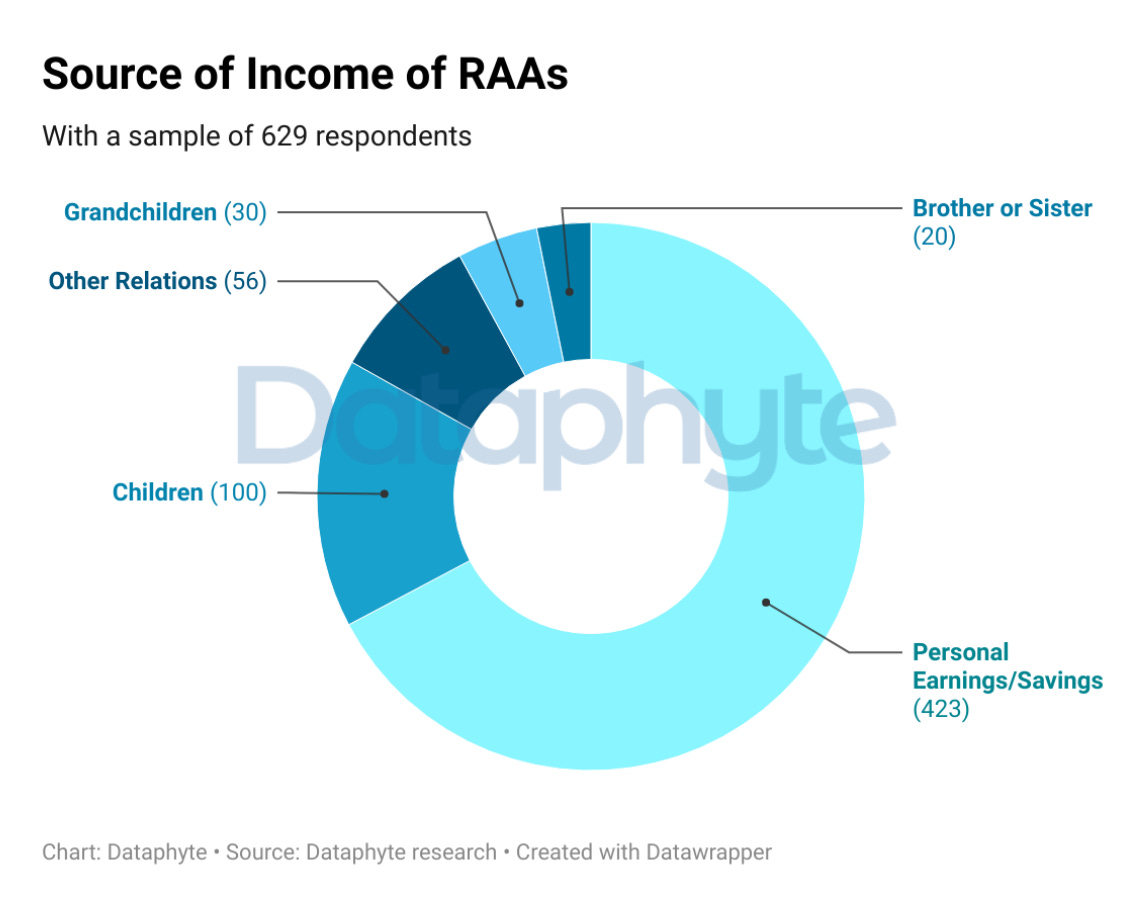

The research conducted by Dataphyte and JAIRAA titled "Access to care and Services for the Retired, Aged, and Ageing Population in Nigeria" states that 67% of all retirees in the study sample live off their savings and earnings, with the remaining 15.9% relying on their children, 8.9% on family, and 4.8% and 3.2% on siblings and grandchildren, respectively.

These savings and earnings by Retired, Aged, and Ageing (RAAs) persons could include that from pension savings. However, some RAAs still engage in mental and manual work to make ends meet.

The study also showed that some elderly and retired individuals do not have sufficient clarity about retirement savings plans.

According to the study, 34% of respondents had a basic understanding of the Pension Commission (PENCOM), the organisation in charge of policing and monitoring the actions of pension fund administrators, while 66% of respondents did not.

Nigeria has a dynamic economy and a fast-expanding population, contributing to the difficulty of providing financial stability for its ageing population.

Pensions and pension plans, which offer people financial security and stability in their later years, are essential elements of retirement income planning.

To guarantee retirees receive a steady income after leaving the workforce involves systematic contributions and fund management.

Pension plan investments might be viewed as protecting future income, but workers often spend their income to settle present bills with little or nothing left to save for the future.

Besides, some do not have pension savings because they work in informal settings or formal settings that do not place them on a contributory pension plan.

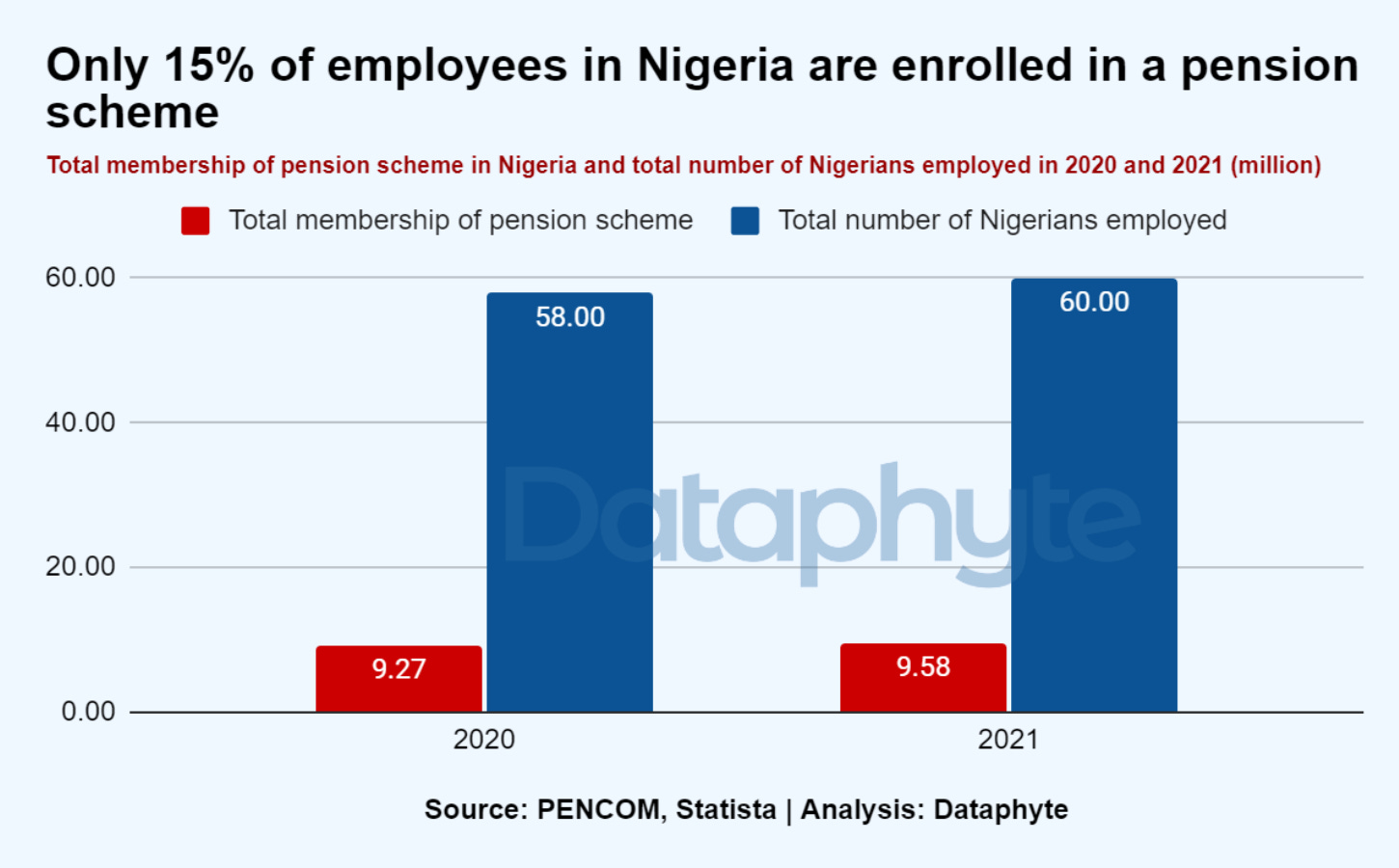

This explains why only 15% of employed Nigerians are members of a pension scheme, according to Pension Commission (PENCOM) and Statista data.

Income Buffers for RAAs

Retirement might feel like a long way off, but the sooner you start saving towards it, the easier it will be.

Pension savings might not be enough in all cases. Additional savings and investments might suffice.

Living by Warren Buffett's wise words, “Do not save what is left after spending, but spend what is left after saving,” is a great mindset to adopt.

Here’s how you can use a Retirement Savings Calculator to help plan for a secure and comfortable retirement with importance to the following information.

Current Age: Your age at the moment

Retirement Age: The age at which you plan to retire.

Life Expectancy: How long you expect to live. A typical estimate could be 85-90 years.

Current Savings: The amount you already have saved for retirement.

Monthly Contribution: How much you plan to save each month from now until retirement.

Annual Return Rate: The annual percentage return you expect on your investments.

Inflation Rate: The expected annual inflation rate, which affects the purchasing power of your money.

Desired Monthly Retirement Income: The amount you want to receive each month during retirement.

You can set and monitor reasonable savings targets and monitor your progress by utilising a retirement calculator and these guidelines.

Retirement security and comfort can be increased by starting early, contributing steadily, and factoring in predicted returns and inflation.