Bank Recapitalisation: 55 Past years and 54 Peers

Pause for a moment!

Have you ever wondered why you hardly hear that a bank has unexpectedly stopped its operations?

Well, it rarely happens. Yet, it can occur.

It's not something we'd wish for. Still, it is a scenario that prompts us to discuss the security of our bank deposits and the stability of banks and other financial institutions.

Banks play a pivotal role in a nation's economy, serving as the cornerstone of its financial system.

A bank's overall growth is determined by the quality of its assets, financial stability, operational efficiency, profitability, return on risk, and general soundness.

So, how strong is your bank? Better still, how safe are your shares and deposits in the bank?

Bank Capital Reviews (1969-2024)

A strong bank typically has robust financial health, including viable capital, sufficient reserves, and manageable levels of risk exposure.

To ensure banks don’t fail easily, Central Banks worldwide stipulate minimum capital requirements. Likewise, the Central Bank of Nigeria (CBN) regulates this minimum capital a bank must possess to operate.

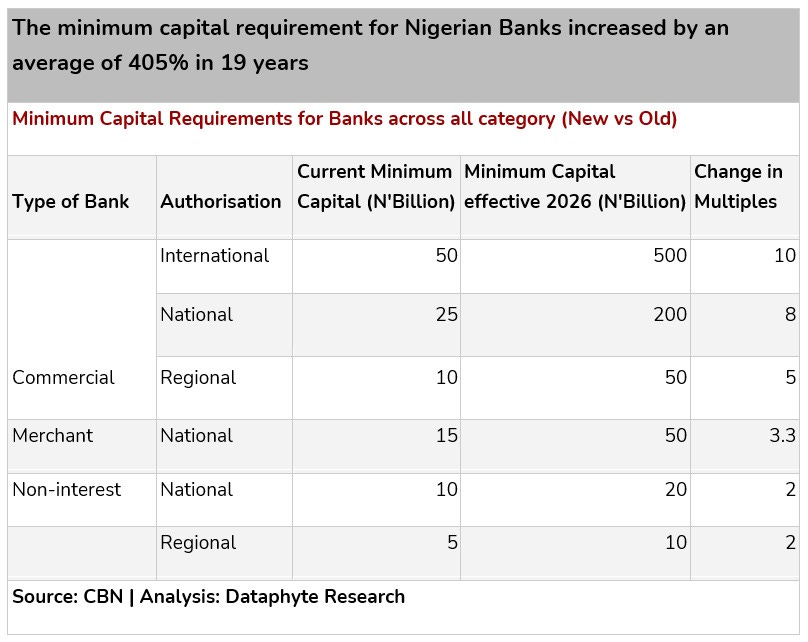

Recently, the (CBN) announced an upward review of all bank capital requirements.

This decision aims to maintain sufficient capital to strengthen banks against external and domestic economic shocks.

The new capital requirement for commercial banks with international licenses was reviewed from N50 billion to N500 billion.

On the other hand, the minimum capital that national banks can hold was adjusted from N25 billion to N200 billion, while that of regional banks increased from N10 billion to N50 billion.

While bank recapitalisation is a norm in the banking sector, the CBN's new review has elicited mixed reactions from stakeholders.

For instance, Rasheed Bolarinwa, President of the Association of Corporate & Marketing Communication Professionals of Banks (ACAMB), expressed support for the CBN circular on banking sector recapitalisation and described it as a much-anticipated exercise.

Conversely, there are concerns that the recapitalisation exercise could result in job losses, particularly in banks that fail to meet the capital requirement after the 24-month implementation period elapses.

This fear stemmed from the last recapitalisation exercise in 2005, which led to massive job losses in banks that could not meet the requirement.

Some banks’ licences were revoked while small and weak banks merged with big banks. This led to the shrinkage of the number of banks existing in Nigeria at the time, from 89 to 25.

Meanwhile, certain factors may make the 2005 recapitalisation programme not directly comparable to 2024.

In 2005, all banks operating in Nigeria were directed to raise their capital from 2 billion to 25 billion. The capital requirement was calculated using all shareholders’ funds, which included paid-up capital, retained earnings, other accumulated incomes or losses, minority shares, and treasury stocks.

For the new recapitalisation, effective from 2026, the apex bank stated that the capital requirements should comprise premium and paid-up capital only.

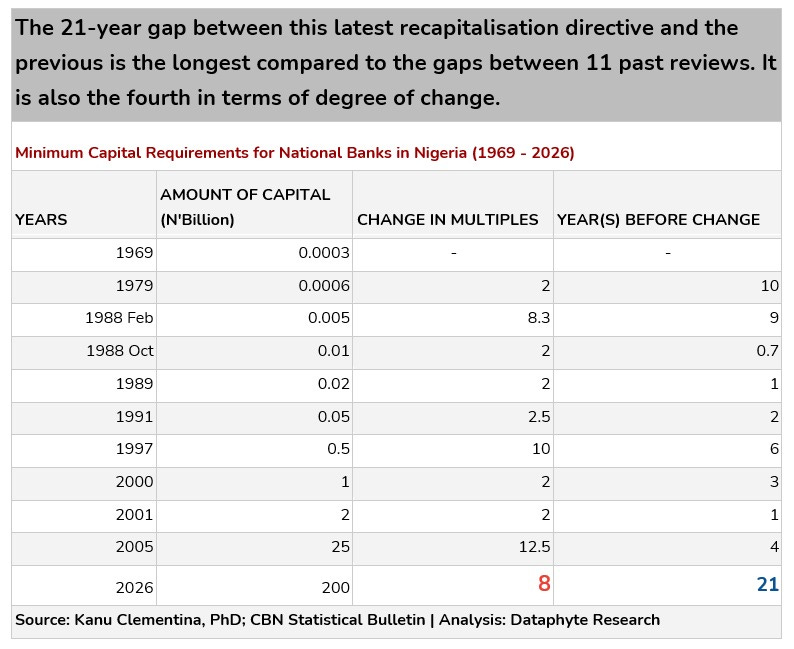

Interestingly, this is the longest Nigerian bank has ever operated without a new recapitalisation. The years between the last recapitalisation and the current one are 21 years.

Also, the new capital requirement, effective 2026, is just 8 times higher than the current one. When compared with peers over the years, it is the 4th highest change in multiples.

Bank Capital Review: 54 African Peers

Do Nigerian Banks really need this much overhauling of their financial strength by the CBN to be viable? Let’s compare them with their peers in 54 African countries and see.

So, aside from having robust capital bases, there are other metrics that determine banks' strength. These multiple factors are reflected in rating the Banker's Top 100 African Banks.

Last year, 11 of the 25 Nigerian commercial banks made the list.

The Banker’s Top 100 African Banks is an annual ranking of banks in selected African countries based on certain parameters, which include overall growth, profitability, operational efficiency, asset quality, return on risk, liquidity, and general soundness.

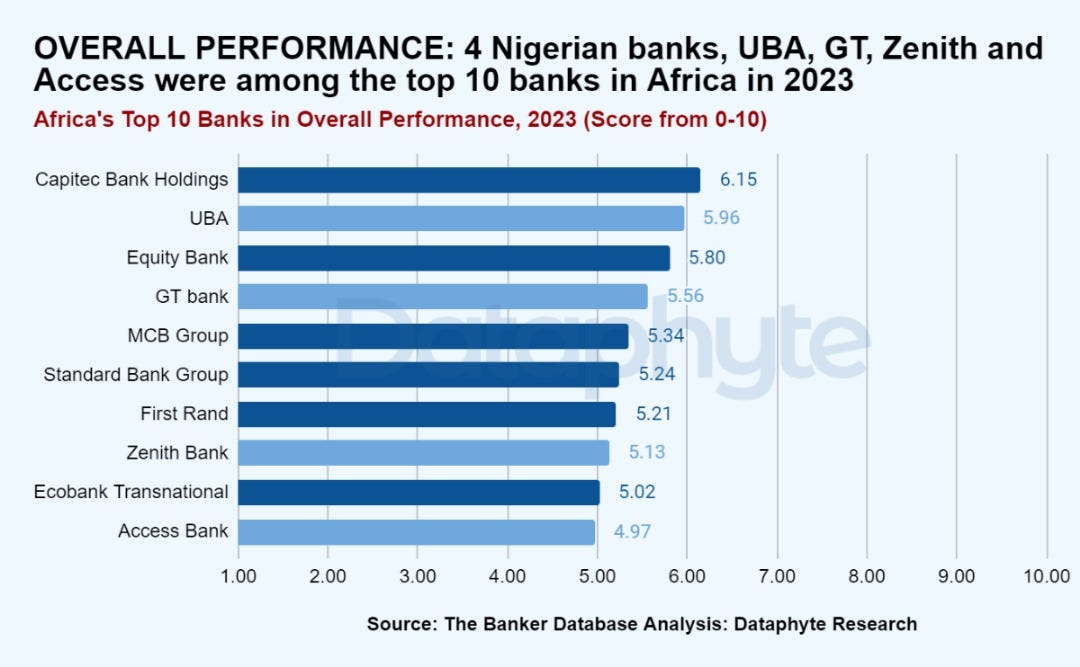

Regarding overall performance, 4 Nigerian banks were among Africa’s top 10 in 2023.

UBA Bank was rated second with a score of 5.96 over 10, after Capitec Bank Holdings of South Africa, which led others with a score of 6.15.

The next Nigerian bank, GT Bank, came fourth with a score of 5.6, and Zenith Bank ranked 8th with a score of 5.1. Access Bank took the last spot among the best 10, with an overall performance score of 4.97.

Interestingly, Nigeria is the only country with the highest representation in this ranking category. Four of its banks made it to the list, with only three from South Africa and one each from other countries present.

Could this mean the Nigerian Banks are doing just fine and do not urgently need recapitalisation, as the CBN directed?

Let’s see further.

Asset Quality

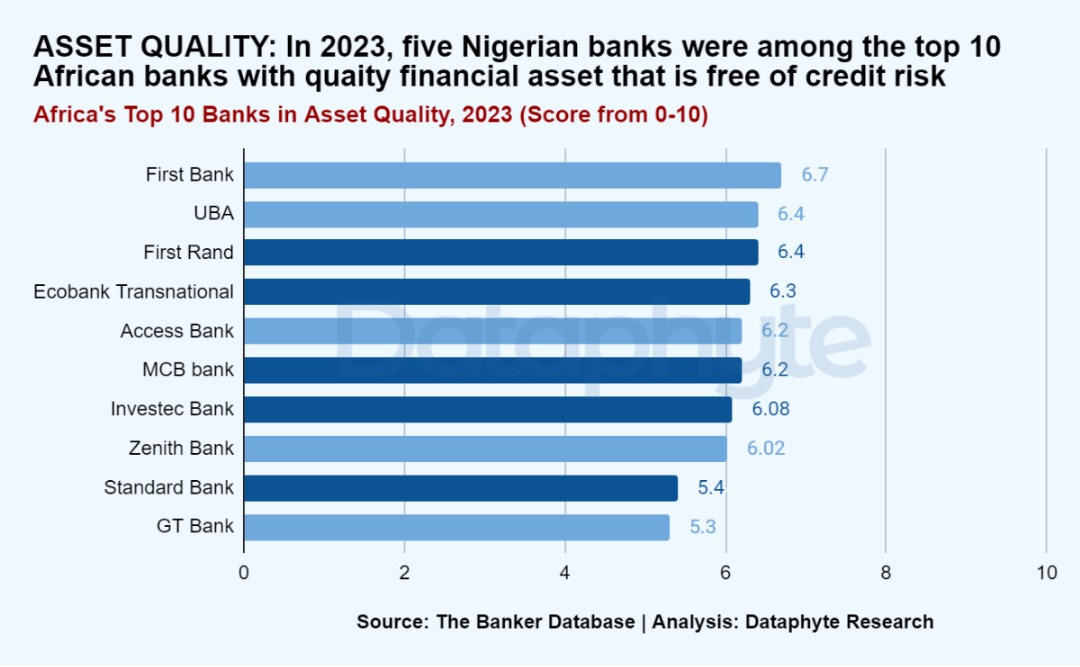

Regarding asset quality, half, that is, 5 of the 10 banks on the top 10 list are from Nigeria. This indicates that these Nigerian banks have healthy financial assets that can withstand credit risk and other risks associated with a bank's lending activities.

Yet, we are talking of only 5 out of Nigeria’s 25 commercial banks. Do these 5 reflect the health of the average Nigerian Bank?

Notably, First Bank and UBA were listed first and second with a score of 6.7 and 6.4 out of 10. Access Bank and Zenith Bank scored 6.2 and 6.02, while GT Bank, which came last on the list, scored 5.3.

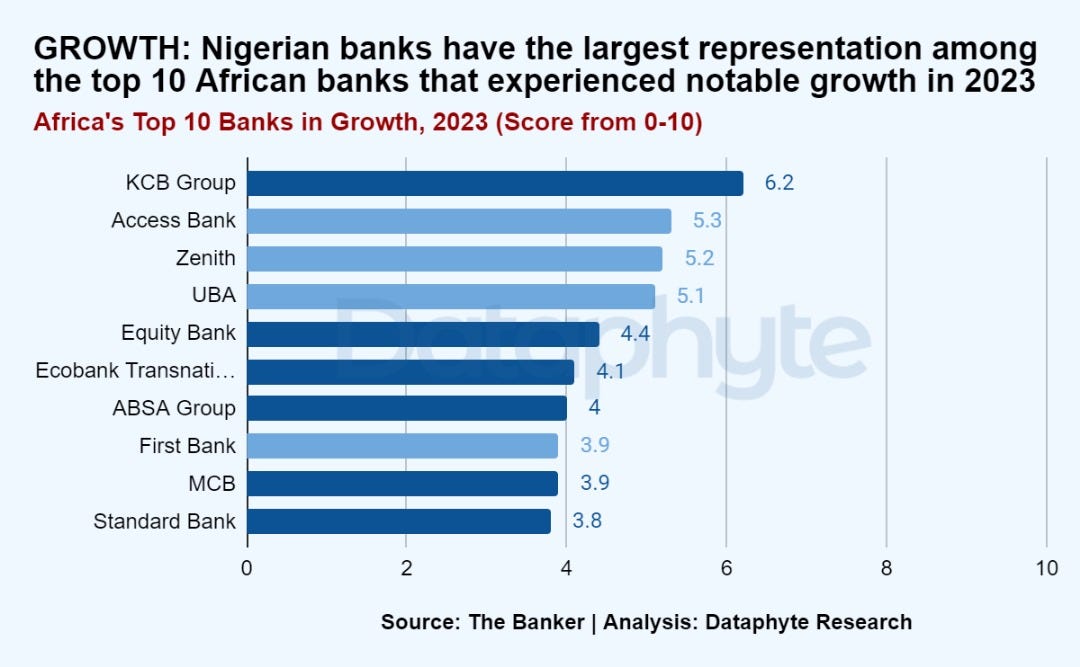

Growth

Similarly, Nigerian banks experienced significant growth in their overall financial performance, with four ranking among the top 10 African banks that recorded growth in 2023

Despite Nigerian banks' strong performance in the three categories discussed, they lag behind their African peers in other financial metrics.

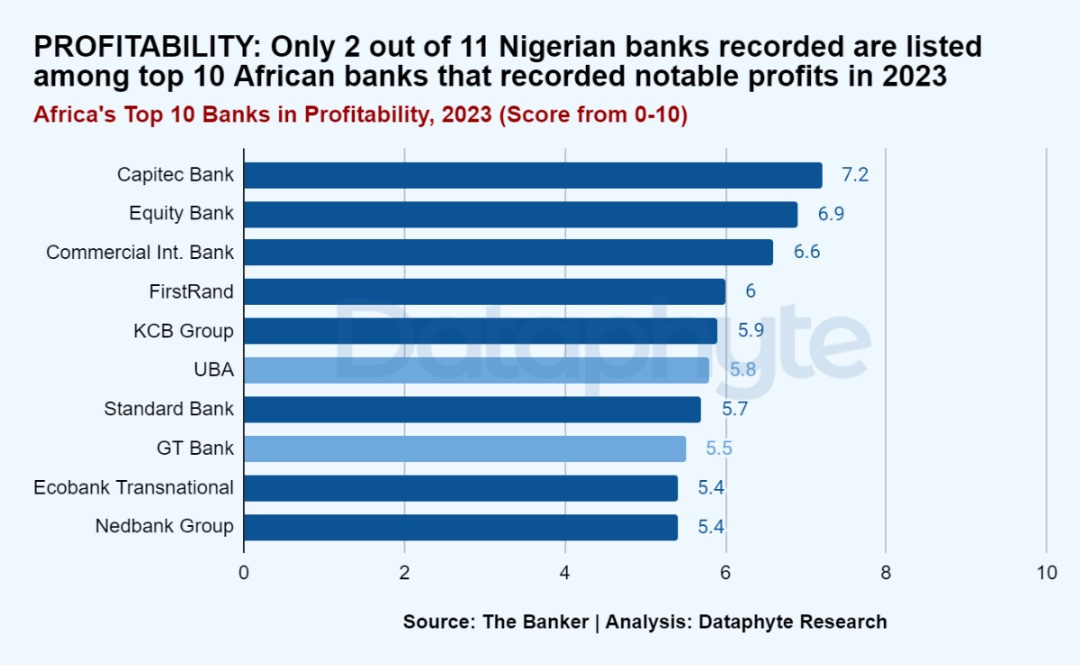

Profitability

Based on their profitability, only two Nigerian banks are listed among the top 10 African banks. This metric describes their ability to generate earnings and returns on their investments and operations, and it is measured by return on assets (ROA), return on capital (ROC), pre-tax profit and others.

Regarding profitability, Nigeria’s top banks aren’t prominent compared to their feats in other financial metrics.

Only UBA and GT Bank made the top 10 profitable banks list.

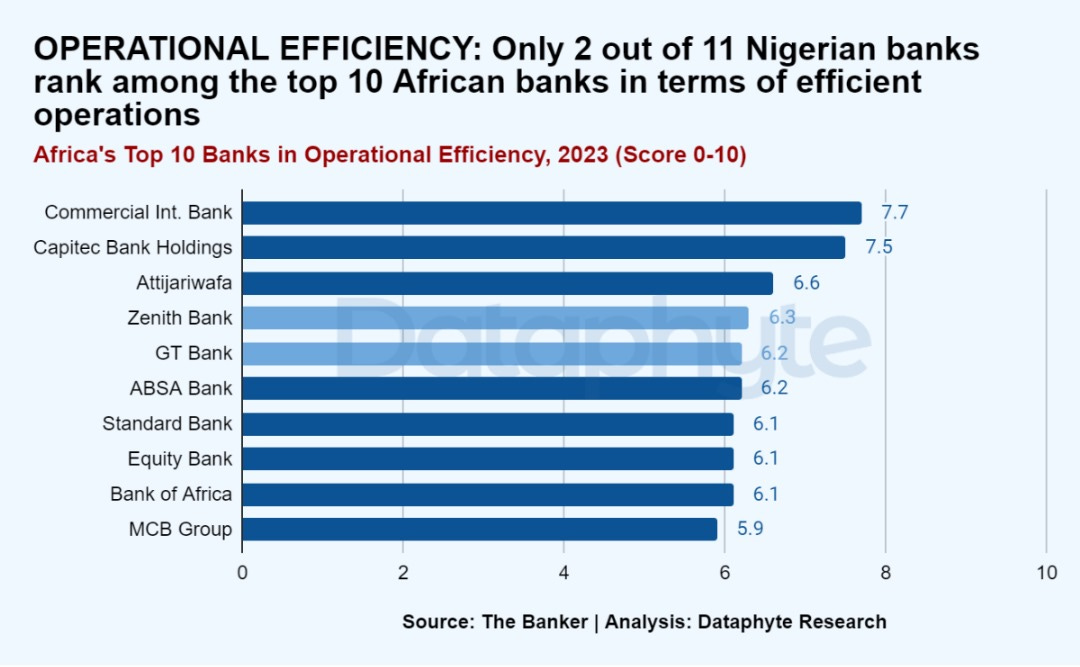

Operational Efficiency

Also, when it comes to reducing costs and enhancing productivity while maintaining or improving returns, only a few Nigerian banks can match their African counterparts.

While 11 Nigerian banks are among the top 100 African banks, only 2 of the 11 are among the top 10 in terms of operational efficiency.

These 2 banks are Zenith Bank and GT Bank.

Can the CBN capital review improve the efficiency of Nigerian banks, both big and small?

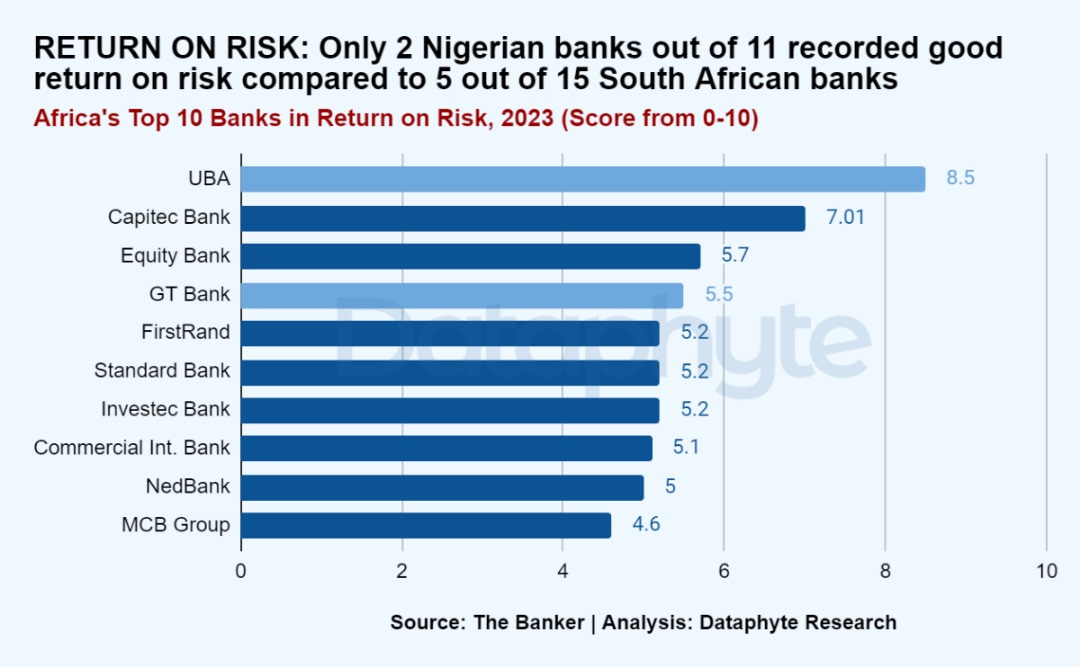

Return on Risk

Meanwhile, only 2 Nigerian banks, compared to 5 South African banks, are among the top 10 African banks that generated good returns relative to the amount of risk they took in 2023.

It’s comforting that UBA led the other 99 African banks in this category and GT Bank was fourth. Yet Nigeria's representation is still relatively low in risk management compared to its performance in asset quality.

So, Nigerian banks are making relative progress when it comes to robust financial assets and potential for growth.

On the other hand, Nigerian banks need to learn from their African peers about effective operations, return on risks, and overall soundness.

Let’s hope this new bank recapitalisation move from Cardi B, sorry, Cardoso’s CBN, helps Nigerian Banks improve all their performance metrics, offering depositors maximum returns on their savings and shareholders sustained returns on their investments.

Hope you enjoyed this Data Dive. It was written by Funmilayo Babatunde, who maintains a close friendship with a tall, dark, and handsome male bank staff whose physique really fits her spec, and edited by Oluseyi Olufemi, who dated a fair complexioned female bank staff, whom he later married.