Cybersecurity Levy: 5 Entities Concerned

Cybersecurity Levy: 5 Entities Concerned

+POS Registration to Curb 18% of Payment Frauds

Cybersecurity Levy: 5 Entities Concerned

The Central Bank of Nigeria (CBN) has directed banks to start deducting a 0.5% cybersecurity levy on all electronic transfers from 5 types of entities.

The new directive to impose a new levy for all electronic money transfers has sparked public outrage following the announcement on Monday, May 6, 2024, that banks operating in the country should start charging a cybersecurity levy on transactions.

However, this levy does not concern individuals and businesses except those specified in Schedule 2 of the Cybercrime (Prohibition, Prevention, Etc.) (amended) 2024 Act.

These 5 business entities are;

GSM Service providers and all telecommunication companies;

Internet Service Providers;

Banks and other Financial Institutions;

Insurance Companies;

Nigerian Stock Exchange

According to the CBN, the levy is intended to implement the funding arrangement stipulated in the Cybercrime Act, which requires the Office of the National Security Adviser to receive funds for preventing and detecting cybercrimes in Nigeria.

According to the Central Bank of Nigeria, all these transactions by individuals and businesses are exempted from the cybersecurity levy:

Loan disbursements and repayments

Salary payments

Intra-account transfers within the same bank or between different banks for the same customer

Intra-bank transfers between customers of the same bank

Other Financial Institutions instructions to their correspondent banks

Interbank placements

Banks’ transfers to CBN and vice-versa

Inter-branch transfers within a bank

Cheque clearing and settlements

Letters of Credits

Banks’ recapitalisation-related funding – only bulk funds movement from collection accounts

Savings and deposits, including transactions involving long-term investments such as Treasury Bills, Bonds, and Commercial Papers.

Government Social Welfare Programmes transactions e.g. Pension payments

Non-profit and charitable transactions, including donations to registered non-profit organisations or charities

Educational institutions’ transactions, including tuition payments and other transactions involving schools, universities, or other educational institutions

Transactions involving bank’s internal accounts such as suspense accounts, clearing accounts, profit and loss accounts, inter-branch accounts, reserve accounts, nostro and vostro accounts, and escrow accounts.

POS Registration to Curb 18% of Payment Frauds

The Corporate Affairs Commission (CAC) has instructed banks to ensure the registration of their customers in the agent banking platform on or before July 7, 2024.

“The Central Bank of Nigeria (CBN) had earlier, through a memo issued on April 30, 2024, directed all non-individuals on the Agent Banking Authorisation to immediately take steps to register their businesses with the CAC in line with Section 863 of the Companies and Allied Matters Act (CAMA) 2020,” the CAC informed.

This directive aims to safeguard businesses and regulate the agent banking industry against recent fraudulent transactions linked to certain POS terminals.

Point-of-sale terminals are e-payment systems that provide alternative financial services to people outside the traditional banking system and automated teller machines (ATMs).

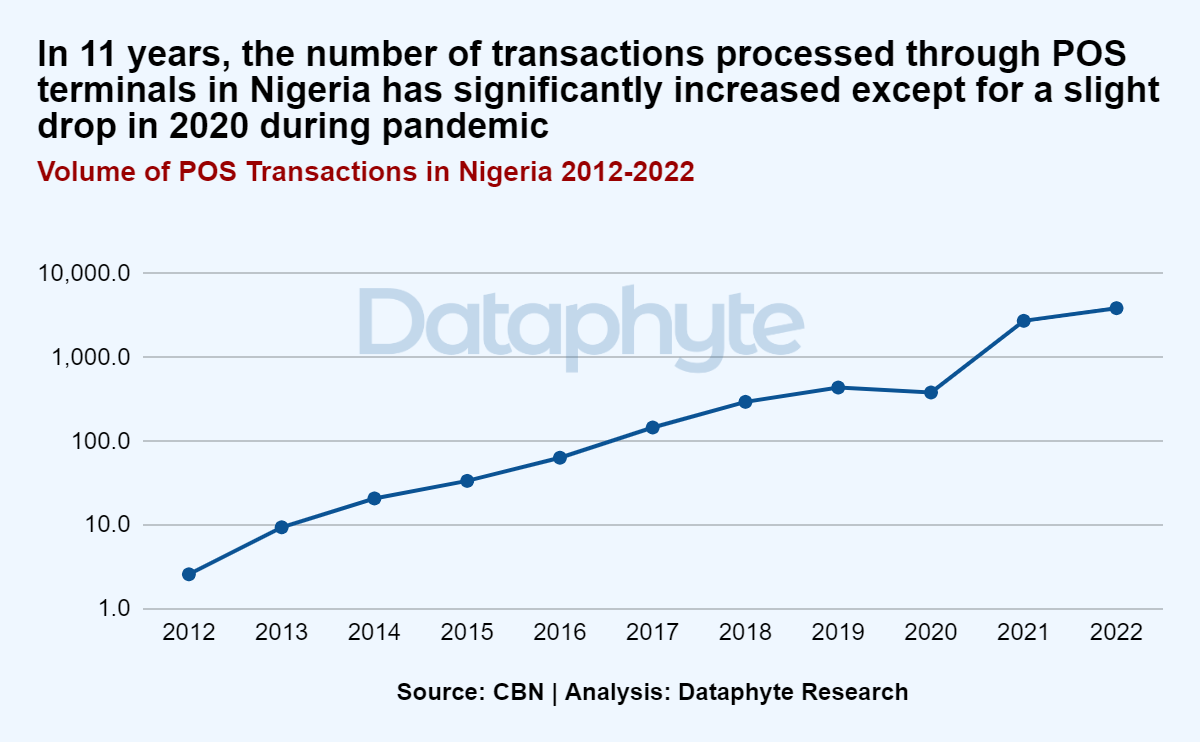

In the last 11 years, the number of transactions processed through POS terminals in Nigeria has significantly increased from 2.6 million total transactions in 2012 to 3.8 billion in 2022.

POS transactions consistently increased over this period, except for a slight drop in 2020 during the pandemic, which later rebounded in 2021 through 2022.

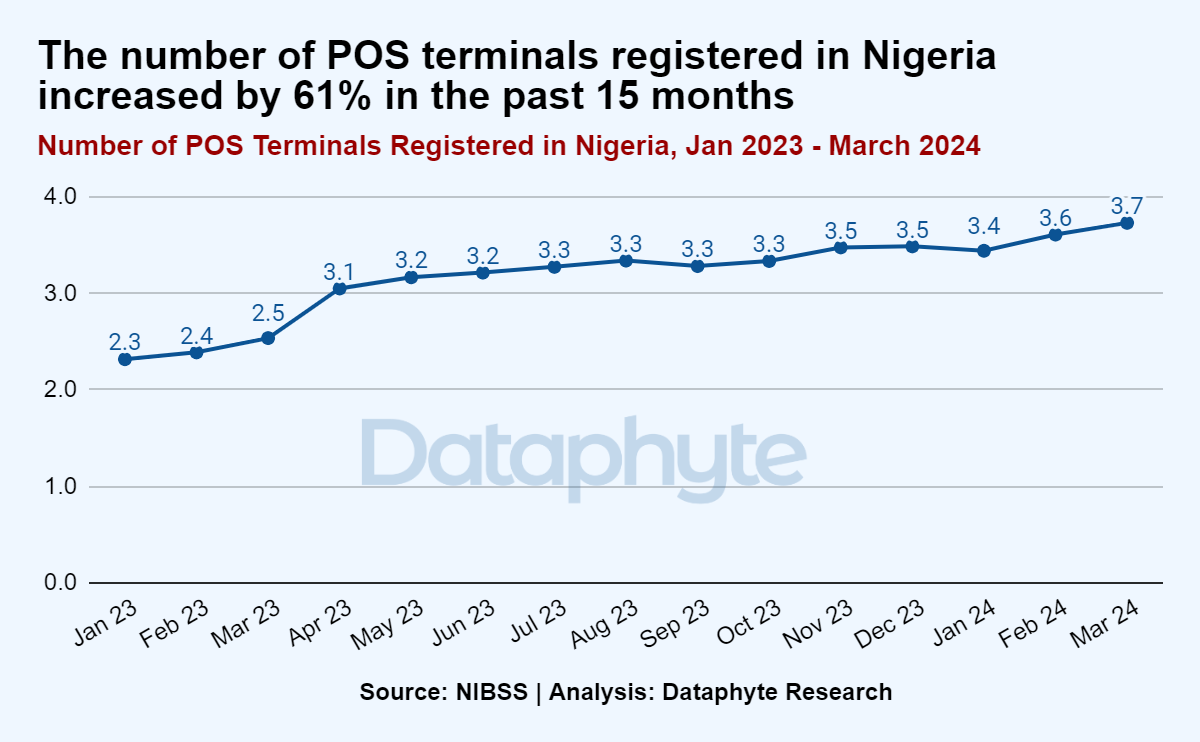

Similarly, the number of POS terminals registered in Nigeria increased by 61% in the past 15 months, from 2.3 million terminals in January 2023 to 3.7 million in March 2024.

This trend indicates a potential growth in electronic payment adoption and a growing preference for POS's alternative financial services.

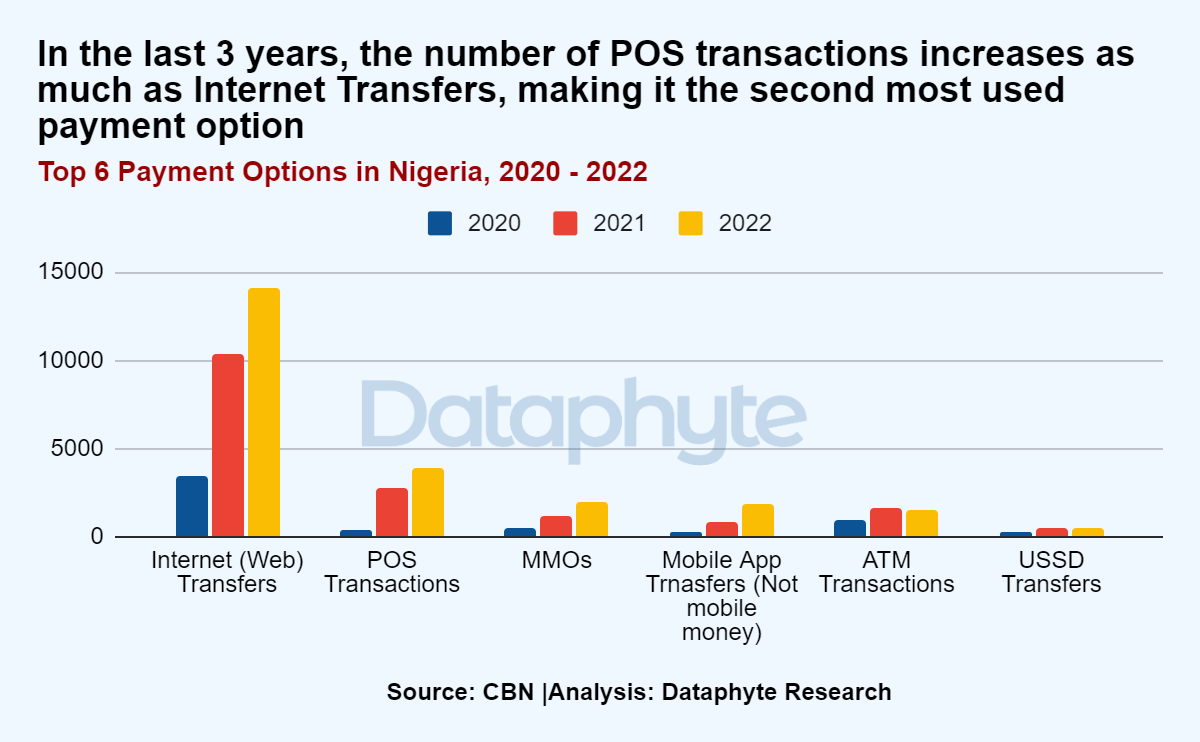

In the last 3 years, the number of transactions through POS has increased as much as Internet Transfers, making it the second most used payment option in Nigeria.

Between 2021 and 2022, there was a 42% increase in POS transactions, rising from N2.7 billion total transactions in 2021 to N3.8 billion in 2022.

Despite the growth of agent banking systems over the years, why does distrust still exist towards their operations?

Should the CBN be concerned?

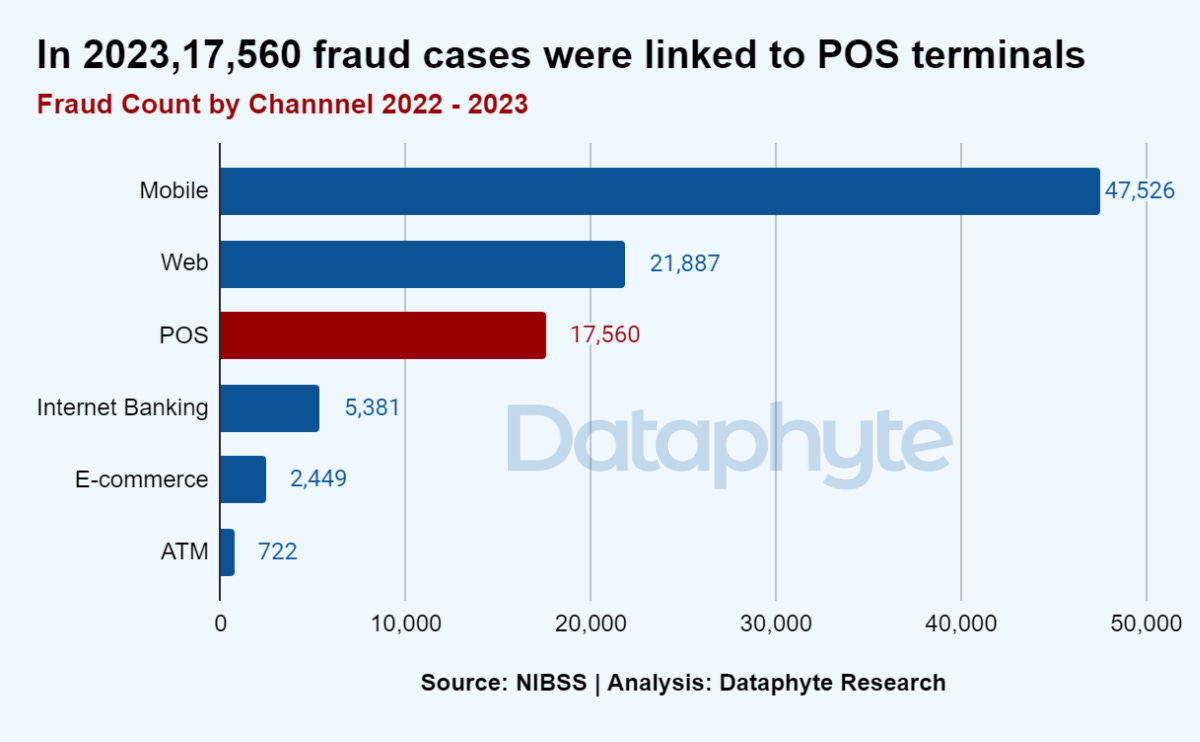

According to the Nigeria Inter-Bank Settlement System (NIBSS) 2023 Annual Fraud Landscape report, the Point of Sale terminal (POS) was fraudsters' second most exploited payment channel in 2023, with a total value loss of about N4.4 billion.

Similarly, an estimated 17,560 fraud cases were linked to POS terminals in 2023.

From 2022 to 2023, the number of fraudulent cases related to POS increased by 8%, while the total value lost to the channel rose by 71.32%.

This prevalent levels of fraudulent activity requires some regulation of the agent banking industry to minimise its susceptibility to fraudulent transactions.

Point-of-sale (POS) businesses have revolutionised access to financial services for millions of people in Nigeria. However, the rising incidence of fraudulent transactions linked to this payment method may spur distrust among consumers and stakeholders alike.

As no payment scheme is entirely immune to fraud, it's crucial to implement stringent regulatory measures to mitigate fraudulent transactions linked to Point of Sale terminals. Identifying common frauds associated with your POS business is essential for maintaining industry safety.

It is hoped that the CBN’s measure will be effective in reducing fraud incidents without reducing access to POS in financially underserved communities.

Thanks for reading this edition of Marina and Maitama. It was written by Funmilayo Babatunde and edited by Oluseyi Olufemi.