Debts, Deficit and Naira’s Dangerous Dance

Debts, Deficit and Naira’s Dangerous Dance

On Wednesday, the Nigerian naira took a scary dance step towards a dangerous direction, sending many Nigerians into a panic mood. After days of heightened interest in its performance, the naira finally crossed the N700 to a Dollar mark as the country continues to suffer a shortage in the supply of the United States’ currency in the foreign exchange (FX) market.

Reports from forex dealers in different parts of Lagos, the nation’s commercial hub, showed that the Naira was exchanged for the greenback at N705/$1, while the hard currency was bought from holders between N697/$1 and N700/$1.

The naira-dollar disparity has raised concerns among Nigerians, creating unease in an already tense social atmosphere. Yet the conversations have remained on the surface, triggering endless “debates” on social media. As analysts and policy experts continue to interrogate the situation, the fundamental drivers of these economic uncertainties have remained largely under-discussed.

Dangerous Deficits, Devastating Results

While the peoples’ obsession with the poor performance of the naira has been quite understandable, the underlying dynamics at play are rather complex. Inevitably, their impact on the overall economy has been devastating.

Last week, the 2022 fiscal performance report for the first quarter of the year showed how the government deficit spending shot up to N3.09 trillion in the first quarter of 2022. The pro rata spending target for the first quarter of the year was N5.77 trillion, while the actual spending as of April 31 was N4.72 trillion. The huge deficit, expectedly, was funded by borrowing.

Interestingly, in the last few years, the nation’s budgets have been built around staggering deficits, a worrisome development that continues to generate ripples among observers and global rating agencies.

For instance, the government’s 2022 budget was projected to be N17.32 trillion, 18 per cent higher than the 2021 budget. Recurrent (non-debt) spending is estimated to amount to N6.91 trillion, which is 40 percent of total expenditure, and 20 percent higher than the 2021 Budget. Aggregate capital expenditure of N5.96 trillion is 35 percent of total expenditure, inclusive of the capital component of Statutory Transfers, GOEs (Government-Owned Enterprises capital), and project-tied loans expenditures. At N3.61trillion, debt service is 21 per cent of total expenditure, and 34 percent of total revenues.

The biggest worry, however, is that even on paper, the budget already has a deficit of N6.26 trillion. With the poor performance in the first quarter, the deficit is bound to shoot up significantly, throwing the nation into more debts.

Now, a breakdown of the actual spending for the first quarter of 2022 showed that N1.94 trillion was for debt service, N1.26 trillion for personnel costs, including pensions.

Shockingly, contrary to the globally recommended fiscal policy position, as at April, only a meagre N773.63 billion had been spent on capital expenditure—despite the huge money borrowed to finance the deficit!

Debt for Consumption

Despite the rising debt profile of the nation, it becomes more worrisome that much of the borrowings aren’t meant to finance infrastructure, or engender production. They are basically for overheads and consumption. Yet the number keeps ballooning.

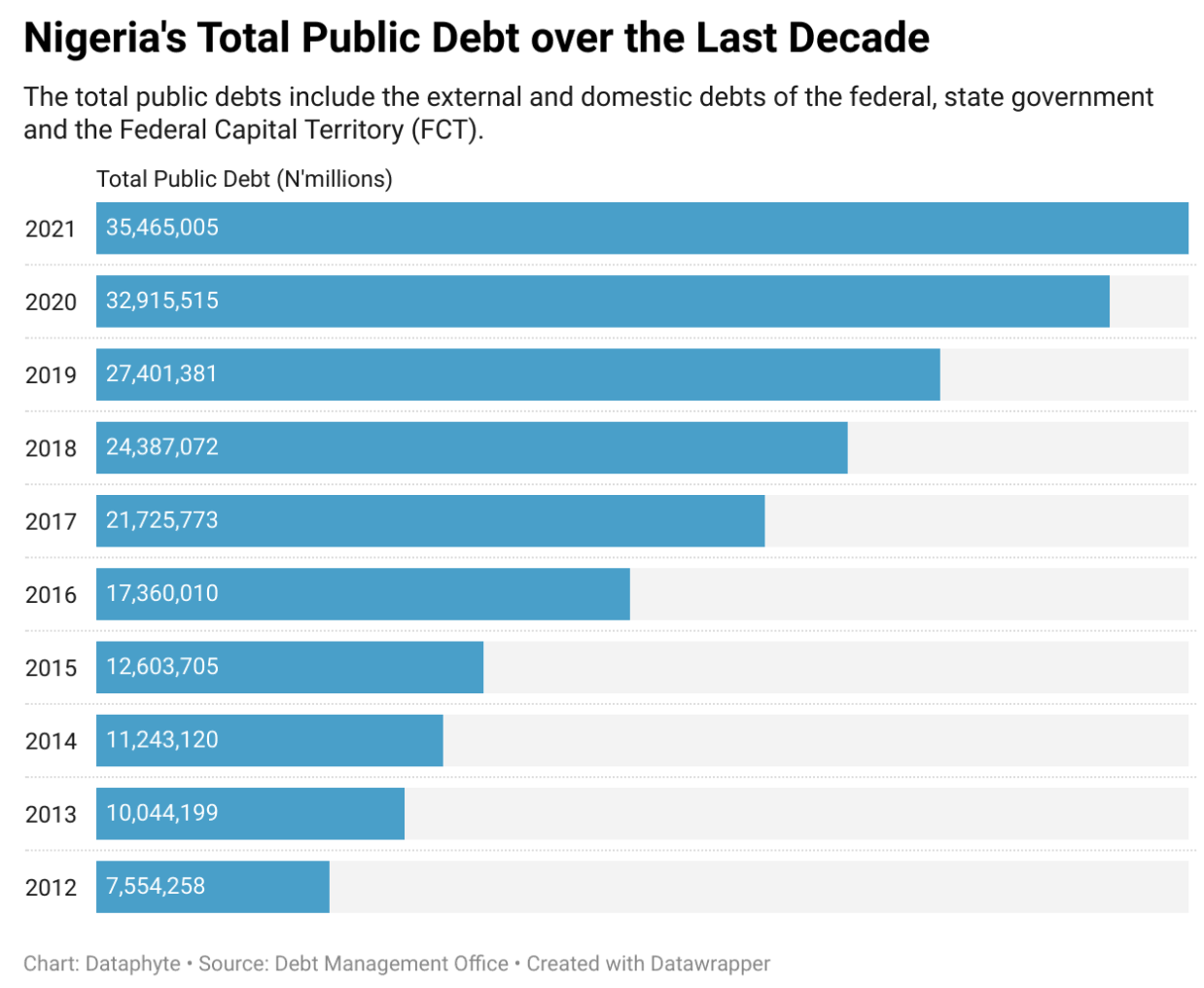

Data from the Debt Management Office shows that Nigeria’s total public debt stock increased to N41.60tn in the first quarter of 2022 from N39.56tn as of December 2021, representing an increase of N2.04tn within a period of three months. The public debt stock covers the total domestic and external debt of the Federal Government and state governments and the Federal Capital Territory.

In dollar terms, while the comparative figures for December 2021 was $95.78bn, it jumped to $100.07bn in March, covering new domestic borrowing by the FGN to partly finance the deficit in the 2022 Appropriation Act, the $1.25bn Eurobond issued in March 2022 and disbursements by multilateral and bilateral lenders.

Although the DMO tries to downplay the nation’s debt worries by insisting that it should be measured in relation to the GDP, analysts have always expressed concerns over such seemingly “dubious” parameters, which ignore a most significant factor like revenue. In the first quarter of 2020, Nigeria's debt service as a percentage of revenue rose to 99%, according to the Medium-Term Expenditure Framework and Fiscal Strategy (MTEF/FSP) report released by the Federal Ministry of Finance, Budget, and National Planning.

To be sure, the nation’s total public debt to GDP is now 23.27 per cent, which is below Nigeria’s self-imposed limit of 40 per cent. But when the debt is benchmarked against the revenue, its an abysmally poor performance that should worry all Nigerians.

Why? Only revenues, and not an illusive ‘GDP’, can be used to pay and/or service debt!

Naira’s dangerous dance; Steady Death

Since the naira crossed the N700 mark this week, people have come up with a plethora of reasons why the nation’s currency has performed so abysmally. From poor monetary policies (of CBN) through arbitrage and all that, it’s been a chaos of alibis.

The biggest takeaway, however, is that the nation’s export potentials remain underwhelming, and the ripple effect would continue to haunt the naira.

Simple economics principle dictates that a country with a high demand for its goods tends to export more than it imports, increasing demand for its currency. A country that imports more than it exports will have less demand for its currency.

According to a data resource website, Nigeria records an annual trade balance of about -$10 billion, as the value of exports has fallen -$45.6 billion over the last seven years, from $97.6 billion to $52 billion.

In March, the CBN said the value of Nigeria’s international trade deficit rose by 175.13 per cent from $152.94m in January 2022 to $420.79m in March 2022. From export of $4.74bn and import of $4.89 in January, the trade deficit stood at $152.94m. The number increased further in February to hit $190.96m, with export at $4.70bn and import at $4.89bn.

Data from the CBN shows that the total value of international trade was $28.77bn in Q1 2022, with imports at $14.77bn and exports at $14.01bn, showing a total trade deficit of N764.69m.

In effect, a rising level of imports and a growing trade deficit portends danger for a country's exchange rate as weaker domestic currency stimulates exports and makes imports more expensive. Conversely, a strong domestic currency hampers exports and makes imports cheaper.

To arrest Nigeria’s debts and deficit crises, the nation must be deliberate about moving from consumption to production, and, in effect, encouraging export. It must also address its taste for foreign items, especially the non-essentials.

The naira’s dangerous dance this week has shown that the road to Sri Lanka isn’t that far away. The dangerous slide must be halted now.

I think more awareness should be made on why naira is reducing in value.

It needs to be clearly stated; *Naira doesn't have value because Nigeria imports more than export.*

Nigeria need to increase value just the same way smart working class people increase their value.