Devaluation and Nigeria’s Debt + Oando’s bold move in Angola

On Tuesday January 21st, the Debt Management Office (DMO) updated Nigeria’s debt position as at September 30, 2024. Its report showed that total debt stock grew to ₦142.3 trillion, up 5.97% from ₦134.3 trillion in Q2 2024. Broken down into its external and domestic components, we see that the naira equivalent of Nigeria’s foreign debt grew by 9.22% from ₦63.07 trillion in Q2 2024 to ₦68.89 trillion in Q3 2024, even though the dollar value of the debt remained largely steady at around $43 billion.

On the domestic side, debt increased from ₦71.22 trillion in Q2 2024 to ₦73.43 trillion in Q3 2024, an increase of 3.1%, while in dollar terms, domestic debt decreased from $48.45 billion in Q2 2024 to $45.87 billion in Q3 2024, a decline of 5.34%.

The increase in the debt stock in Naira terms is largely due to a decline in the Naira’s value, as it moved from $1,470 in June 2024 to $1,610 in September 2024, a decline of 9%. Throughout 2024, the Naira was on a consistent downward trend, so much so that it was one of the world’s worst performing currencies in 2024, losing 82% of its value as at October 2024 when compared to the start of that year.

The DMO’s update for Q3 2024 raises two main issues. First, the importance of stabilizing the currency. There are many advantages of a stable currency like overall price stability and as an incentive for investment, but in this specific case, a stable currency means that the country’s foreign debt does not explode in Naira terms, burdening the country by reducing fiscal space due to increasing debt servicing commitments.

Secondly, with debt servicing now well over 100% of government revenue, it is past time to insist on genuine economic progress for all the debt being taken on. The Q4 debt profile update from the DMO will include the $2.2 billion Eurobond that was finalized in December 2024. This Eurobond will take foreign debt to over $45 billion, and total debt stock to north of ₦146 trillion.

Given the already precarious state of government finances and perennially slow growth, it is difficult to see how this level of debt will be sustainable. It is time to demand answers.

Charting New Horizons: Oando's Bold Move in Angola's Kwanza Basin

Oando Plc announced that the Angola National Agency for Petroleum Gas and Biofuels (ANPG) awarded its upstream subsidiary, Oando Energy Resources (OER), operation of Block KON 13 in Angola's onshore Kwanza Basin, following a competitive bidding process.

This marks a significant shift in Oando’s operations, aligning with its long-term vision of growing its upstream operations across Africa.

This development could enhance investor confidence, improve the valuation and performance of Oando's stock, and potentially increase its market share within Nigeria's oil and gas industry.

In 2024, Oando achieved full ownership of Nigeria Agip Oil Companies (NAOC), resulting in a significant surge in its share price by ₦50.45. The stock rose from ₦15.55 in July 2024, before the acquisition in August 2024, to ₦66 by the end of December 2024, making it the 3rd highest gainer on the Nigeria Stock Market (NGX) in 2024.

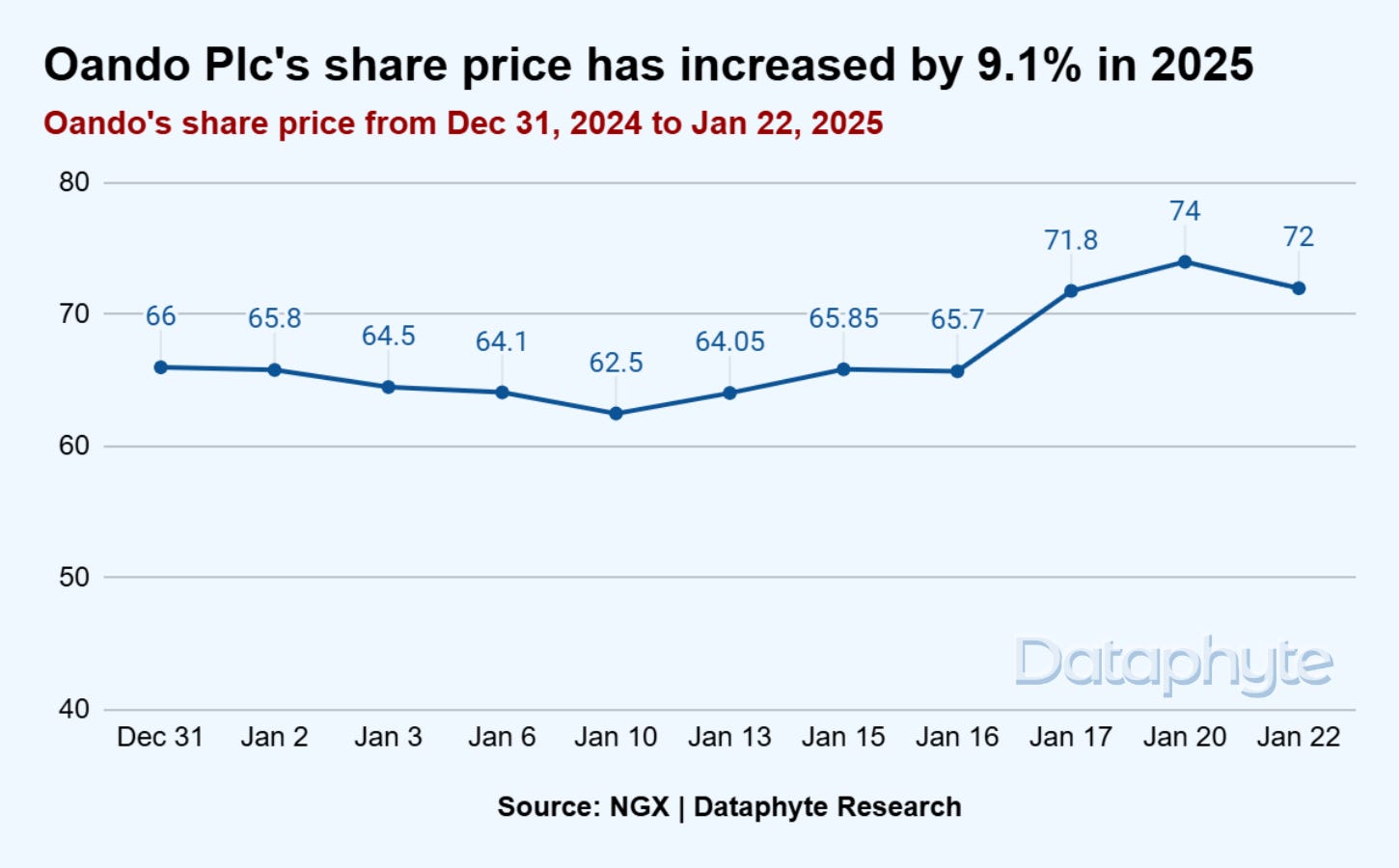

In the first 22 days of January 2025, Oando's share price has increased by 9.1%, rising from ₦66 on December 31, 2024, to ₦72 as of January 22, 2025.

According to its Financial Statement released in November 2024, revenue grew by 51% between the first half (H1) of 2023 and the first half of 2024, increasing from ₦1.3 trillion in H1 2023 to ₦2 trillion in H1 2024. However, profit after tax declined from ₦112.4 billion in H1 2023 to ₦62.6 billion in H1 2024.

These prolific acquisitions have raised its valuation and increased its market share in the oil and gas sector within one year. The valuation/market capitalisation of the company increased by 656%. It moved from ₦112.5 billion in 2023 to ₦895 billion in 2024.

Oando currently holds a 12% market share in the oil and gas sector, making it the third-largest player in this industry segment on the Nigerian Stock Exchange.

Investors may perceive this acquisition as an opportunity for future revenue growth. The Kwanza Basin holds significant untapped reserves, and successful exploration and production could bolster Oando's profitability.

The anticipation of long-term financial gains could make Oando’s stock more attractive to investors.

Block KON 13 is strategically situated in the resource-rich Kwanza Onshore Basin, offering substantial exploration potential in both pre-salt and post-salt plays, with estimated prospective resources ranging from 770 to 1,100 million barrels of oil. The block features two exploration wells previously drilled to a depth of 3,000 meters, with oil and gas identified across various depths.

Oando Energy Resources (OER) holds a 45% participating interest and will serve as the operator for the block, in partnership with Effimax (30%) and Sonangol (15%) as co-venturers.

The Group Chief Executive, Oando Plc, Wale Tinubu CON, stated, “I am thrilled by our successful bid and award of Block KON 13 in Angola. This development underscores Oando’s relentless commitment to expanding our footprint across Africa and contributing to the continent’s energy-sufficiency goals. I am confident in our ability to leverage our expertise to develop and maximise the value of this asset. We look forward to collaborating with our co-venturers and other key stakeholders to harness this opportunity and unlock its full potential for Angola and Africa as a whole.”

In addition, in 2024, Oando was shortlisted among the final three contenders for the acquisition of Trinidad and Tobago's $15 billion Petrotrin Refinery.

Having begun the year on this note, 2025 might be another great year for Oando and its shareholders.

Thanks for reading this edition of Marina and Maitama. It was written by Lucy Okonkwo, and Joachim MacEbong.

If you've read this far, now take 2 seconds to share:

Invite your friends and earn rewards

If you enjoy Marina and Maitama, share it with your friends and earn rewards when they subscribe.