Insecure Businesses

The top twelve Nigerian states with the best infrastructure, all located in the northeast and northwest regions of Nigeria, attracted no foreign investment in 2023.

Coincidentally, all the 12 states record the highest indicators of insecurity.

Persistent security challenges in some areas of Nigeria outweigh the benefits of advanced infrastructure or the potential of a large market for intending investors.

Investors prioritise safety, and areas with reported insecurity may deter foreign capital despite the physical amenities in place.

Several states in Nigeria have consistently ranked high in terms of infrastructure development. States like Kebbi, Yobe, Gombe, and Bauchi have invested significantly in road networks, power supply, and other essential facilities.

Despite these advancements, these states find themselves in the unexpected position of not attracting foreign investments commensurate with their infrastructure status.

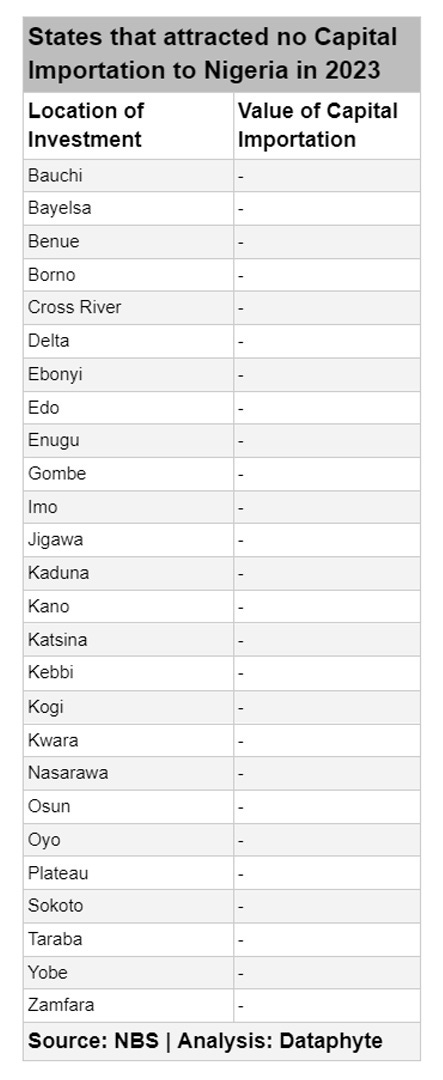

All states in the northeast region of Nigeria except Adamawa did not attract any foreign investment in Nigeria.

Over five years, 8 out of these 26 states have had no capital importation. Between 2019 and 2023, three states in the northeast; Gombe, Taraba, and Yobe, attracted no capital importation, and Jigawa, Kebbi, and Zamfara in the northwest also did not attract any capital importation.

While Bayelsa and Ebonyi, in the South-South and South-East, had no capital importation.

During the year under review, Lagos, Abuja, and Abia top the list of states with the highest capital importation attraction. With only 11 states and the FCT attracting the $3.9 billion of the total capital importation Nigeria got in 2023.

Persistent insecurity in these regions has not only led to the loss of lives and properties, but it also discourages potential investors and reduces the efficiency of investments.

This states that despite the level of infrastructure of these states, investors are not willing to take the risk of investing in these states due to the high level of insecurity.

According to a study on “Insecurity and Patterns of Foreign Direct Investment in Nigeria (1999-2014),” it held that empirical studies dictate that the loss of foreign investors’ confidence occasioned by security challenges would prompt large outflows of capital in affected countries.

Also, the fact that a country is branded a security risk because of the high level of insecurity features like militancy, ethno-religious violence, terrorism and insurgency, would make it less attractive to FDI.

A Declining FDI and Increasing Unemployment

Nigeria is grappling with a concerning economic scenario as its foreign direct investment (FDI) took a staggering 83% plunge over the past decade, reaching $377.38 million in 2023.

Concurrently, the unemployment rate has surged to 5.0% in the third quarter of 2023, reflecting a 0.8% increase from Q2.

The drastic decline in FDI raises alarming concerns about the country's economic appeal to international investors, impacting various sectors including job creation in the country.

The spike in unemployment adds a layer of complexity to Nigeria's economic challenges.

Nigeria’s foreign direct investment in 2023 shows an alarming decrease, with a total of $377.38 million. Nigeria's Foreign Direct Investment Fell by 83% in 10 Years. This suggests that the country’s economic conditions are perceived as unattractive to foreign investors.

In the third quarter of 2023, Nigeria's unemployment rate surged to 5.0%, a rise of 0.8% above the rate from the previous quarter.

The decline in FDI suggests a diminishing confidence in Nigeria's economic conditions among foreign investors, contributing to the country's unattractiveness on the global stage.

This, coupled with an increase in unemployment, points towards a potential economic downturn.

FDI is a key driver of job creation, and the plummeting investment levels indicate a significant reduction in opportunities for local labour.

The Chukwu et al research "Effect of capital importation on Nigeria economic growth" underscores FDI's positive impacts, including cash influx, technology transfer, and job creation, all of which are critical for economic growth and stability.

The interplay between dwindling FDI and rising unemployment emphasizes the urgent need for strategic economic reforms.

Chukwu et al's research highlights the potential benefits of FDI, such as increased productivity and improved human capital.

Nigeria's challenge lies in reversing the downward trend in FDI, implementing policies that attract foreign investors, and simultaneously fostering skill development to mitigate the escalates unemployment rates.

The dynamic relationship between FDI and unemployment underscores the importance of comprehensive economic strategies to navigate these challenging times.

Debts in the Capital

The Federal Capital Territory Administration (FCTA) in Abuja is in the spotlight as 43 embassies and key government entities, including the Presidential Villa and various Ministries, Departments, and Agencies (MDAs), face a financial reckoning due to substantial outstanding debts.

On February 13, 2024, the FCTA revealed a list of 43 embassies collectively owing $5.3 million in ground rent.

Simultaneously, the Abuja Electricity Distribution Company (DisCo) announced plans to disconnect electricity services to the Presidential Villa and 86 Federal Government MDAs, citing N47.195 billion in unpaid bills as of December 2023.

The FCTA's list publication and the DisCo's disconnection intentions were unveiled on February 13 and February 19, 2024, respectively.

The issue extends back to September 2023 when the FCT Administration reminded entities of their ground rent payment obligations.

The financial distress is centred in Abuja, Nigeria's capital, affecting diplomatic missions, the Presidential Villa, and various government offices.

The embassies and government entities are grappling with mounting debts related to ground rent and electricity bills. The FCT Administration had previously issued reminders about payment obligations, dating back to September 2023.

The FCTA took proactive measures by publishing the list of embassies with outstanding ground rent, signalling a commitment to addressing the city's financial challenges.

Simultaneously, the DisCo issued warnings to disconnect electricity, shedding light on the severity of the debt crisis.

The debt crisis extends beyond government entities, as Ajaokuta Steel Company Limited (ASCL) faces a suspension notice from the Transmission Company of Nigeria (TCN) for N33.71 billion in outstanding energy debt.

However, President Bola Tinubu intervened, ordering the payment of N342 million owed to the Abuja Electricity Distribution Company. Additionally, the State House Management reconciled their debts with the DisCo, disputing the initially published N923 million bill and asserting a N342 million outstanding amount.

This debt situation highlights the pressing need for financial responsibility and management in Abuja's diplomatic and political circles, with possible consequences for basic services and overall economic stability.

Thanks for reading this edition of Marina and Maitama. It was composed by Khadijat Kareem.