Nigeria’s Public Debt Crises, its Private Creditors, and Civil Society Concerns

Nigeria’s increasing patronage of private creditors to finance its budget deficits has reached a crisis point with dire fiscal consequences, new research by the Civil Society Legislative Advocacy Centre (CISLAC) reveals.

Centred on the “Increasing Role of Private Creditors in Nigeria’s Debt Crisis and its Human Costs”, the study worries that “A growing proportion of external debt owed to private creditors under opaque terms and often subject to high-interest rates are contributing to spiralling debt servicing costs, increasing the risks to Nigeria's economy.”

Beside the fiscal distress resulting from the country’s indiscretion toward private debts, these heavy burden of debts reduce availability of funds for social capital such as education and health, which are constitutional rights of the people in Nigeria.

While multilateral and bilateral loans usually come with conditions that restrict the government’s wasteful spending of borrowed funds, private creditors do not care if the loan they granted is misspent; as long as the country does not default on paying back its higher interest rates within a shorter loan repayment period.

One of the controls of the World Bank, for instance, is that the government deficit should not exceed -3 percent of the country’s gross domestic product (GDP). Yet the incumbent federal government has exceeded this limit in 4 years.

“While private lending appears, on the surface, to be devoid of some of the conditionality that comes with multilateral borrowing, which often requires the borrowing governments to commit to policies for economic, political, and financial adjustments to minimize the need for borrowing as well as the risks of default, the actual cost of private borrowing, including the extremely high-interest rates and other related conditions make sustainability a challenge”, the CISLAC study noted.

The first concern is the government’s secret loan terms and poor spending drive

A more significant worry is that the terms of the loans Nigeria sources from private creditors across the globe are shrouded in secrecy.

“In 2021, the Nigerian parliament approved the borrowing of the sum of 6.1 billion dollars for augmenting the national budget, mostly to be borrowed through Eurobonds in the international capital market at costs and with conditions that are kept secret.

“The concern is that this new frontier of lending (private creditors) operates to increase the cost of debt servicing while restricting governments' fiscal strength and constraining their ability to respond adequately to social and economic emergencies brought to the fore by the outbreak of the Covid-19 pandemic”, the study further showed.

Due to its poor management of the public debt, revenues and expenditures, the Buhari administration is ranked lower than the previous administration in managing the country’s economy and finances by the World Bank.

The Buhari government has grown Nigeria’s public debt stock from N12.60 trillion (USD 65.43 billion) in December 31, 2015, to N42.84 trillion (USD 103.31 billion) as of June 30, 2022. The Debt Management Office (DMO) press release explains the current debt burden, thus:

The Total Public Debt Stock, representing the Domestic and External Debt Stocks of the Federal Government of Nigeria (FGN), the thirty-six (36) State Governments and the Federal Capital Territory (FCT), was N42.84 trillion (USD103.31 billion) as of June 30, 2022

The Total External Debt Stock was USD40.06 billion (N16.61 trillion) as of June 30, 2022.

Over fifty-eight percent (58%) of the External Debt Stock are concessional and semi-concessional loans from multilateral lenders such as the World Bank, International Monetary Fund, Afrexim and African Development Bank and bilateral lenders including Germany, China, Japan, India and France.

The Total Domestic Debt Stock as of June 30, 2022, was N26.23 trillion (USD63.24 billion) due to New Borrowings by the FGN to part-finance the deficit in the 2022 Appropriation (Repeal and Enactment) Act, as well as New Borrowings by State Governments and the FCT.

The Total Public Debt to GDP as of June 30, 2022, was 23.06% compared to the ratio of 23.27% as of March 30, 2022, and remains within Nigeria’s self-imposed limit of 40%.

While the FGN continues to implement revenue-generating initiatives in the non-oil sector and block leakages in the oil sector, Debt Service-to-Revenue Ratio remains high.

Interestingly, the June 2022 press release did not state the “high” Debt Service to Revenue Ratio, as it did the 23.06% Debt to GDP ratio.

This is because Nigeria’s debt servicing costs have grown over the years to exceed the Federal Government's revenue collected.

The second concern is the outrageous costs of loans from private creditors

Nigeria’s cost of servicing loans now gulps all its collected revenues, and by the first quarter of 2022, the country’s actual revenues could not match its loan obligations.

This debt crisis is further compounded by the government’s payments of outrageous loan interest rates to its private creditors, that is, the commercial bondholders.

The CISLAC study decried the government’s overreliance on Private Credit, noting that servicing the commercial loans cost much more than the cost of servicing all the other loans combined.

Source: DMO; CISLAC Report

Although private creditors' loans currently constitute 40% of Nigeria’s external debt stock, due to the high-interest rate, 70% of external debt servicing goes to commercial creditors leading Nigeria to spend 90% of its actual revenue on debt servicing.

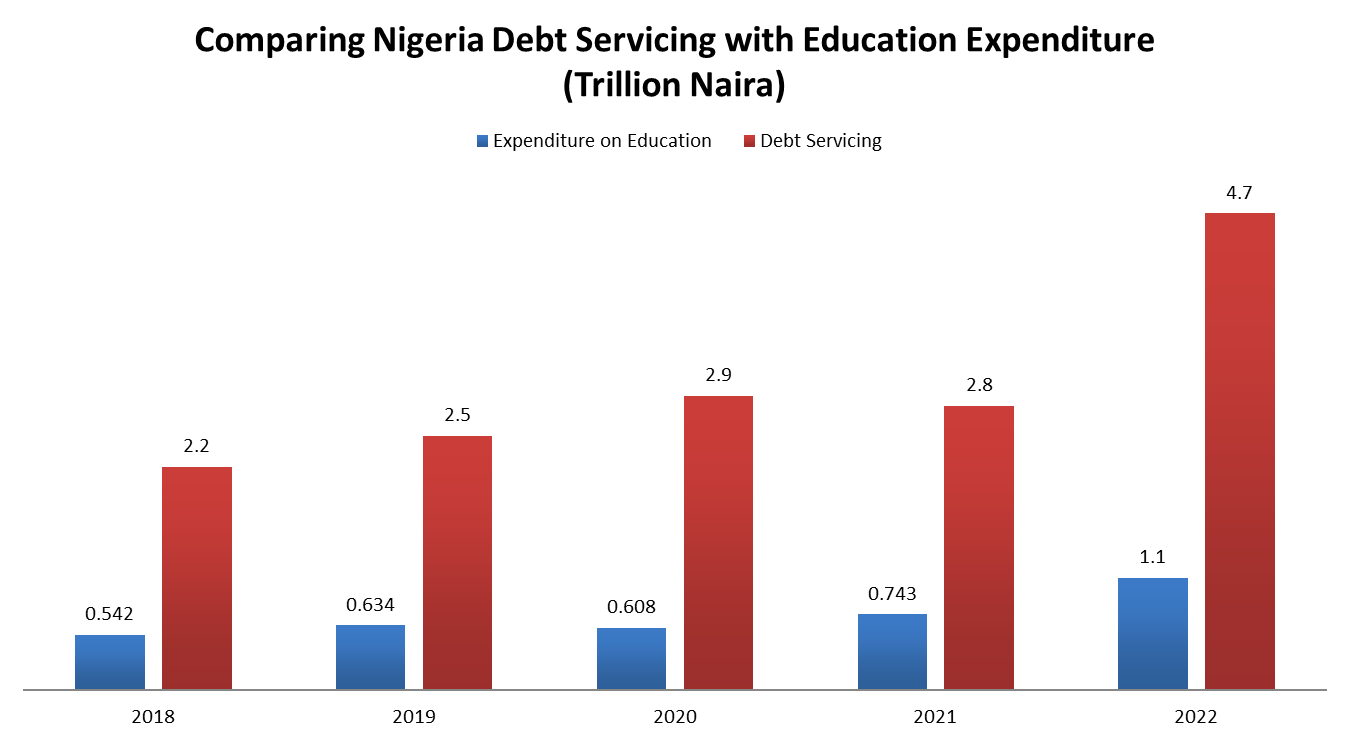

The third concern is the detrimental effect of debt servicing on the government’s social investments

Data shows that Nigeria’s cost of servicing debts far exceeds its expenditure on education and health combined.

Botti Isaac, presenting the research findings, suggests that “The Debt Overhang Theory helps explain how the high cost of servicing the huge public debt in Nigeria is affecting investment in critical sectors that can sustain growth even with consistent and persistent budget deficits”.

Source: DMO; CISLAC Report

The researchers regret that Nigeria diversified to borrowing from private creditors at ridiculous interest rates because it can no longer access concessional loans:

“The real cost of our debt mismanagement is the public services that we fail to get, the facilities and infrastructure that we lose and the subsequent impact on women and children especially. This is a burden for many.

They further chide the government’s reluctance to rein in its fiscal excesses even when it imperils the social development of the citizens and further hinders their economic growth:

“While provisions in the Fiscal Responsibility Act (FRA) sets out fiscal discipline to checkmate the activities of our leaders, they always have a way around it, one of which is shifting the debt threshold from 20% to 40%.

“This raises several questions. Is this the best we can do at the moment? Is the Debt management office responsible for setting the debt threshold? Whose responsibility is it to do this? Should the debt limit be based on our Gross Domestic Product (GDP) or on internally generated revenue (IGR)? What are these debts used for in the first instance?

“Again, the Fiscal Responsibility Commission (FRC) has the responsibility of setting debt limits rather than the DMO since they are the actual borrowers and have the responsibility of ensuring that interest rates for concessional loans should not exceed the statutory 3%. Debt limits should be set on Revenues rather than using a vague concept. Most states are in debt, and it has become vital for states to first obtain a clean bill of health from the Securities Exchange Commission (SEC) and the FRC before applying for loans.

The report echoes the remarks of Victor Muruako, Chairman of the Fiscal Responsibility Commission (FRC), on the pernicious debt crisis:

“It is urgent and imperative, in (the) context of the Country's escalating and spiralling debt stock, that all relevant stakeholders in the debt management space, including civil society, work together to help the Minister of Finance advice the President to fix the debt limits and forward same to the National Assembly for approval as a critical first step in order to achieve debt sustainability in Nigeria.”