On Tinubu’s One Year in Office

Economy, Employment, and other Entanglements

May 29, 2023, the newly sworn-in president, Bola Ahmed Tinubu, in his inaugural speech, promised to “remodel the Nigerian economy to bring about growth and development through job creation, food security and an end to extreme poverty.”

In the maiden edition of the Federal Executive Council meeting, the Minister of Finance and Coordinating Minister for the Economy, Mr Wale Edun, unveiled President Bola Tinubu's three-year eight-point agenda for turning the economy around.

The agenda focuses on 8 socio-economic priorities, 5 of which are directly economic goals:

Food security (Economic)

Poverty alleviation (Economic)

Economic growth and job creation (Economic)

Access to capital, particularly consumer credit (Economic)

Inclusivity in all its dimensions, particularly as regards youths and women (Social)

Improving security (Social)

improving the ease of doing business (Economic)

Improving adherence to the rule of law, and fighting corruption (Social)

Official reports on the first one year of Tinubu's Presidency show that his management of these 5 economic priorities only deepened the straits of the vulnerable masses just as his outlined plans for the economy have lined up the people in various financial entanglements.

According to data released by the National Bureau of Statistics (NBS), under the Tinubu administration, the inflation rate rose to unprecedented levels of price instability in the last 14 years.

This further impoverished the people rather than alleviate their poverty.

This is coupled with a depleted workforce, as the unemployment rate increased to 5%, the highest since Mr Tinubu assumed control of the economy, according to unemployment data from the NBS.

Notwithstanding, this depleted workforce, with depleted wages and depleted welfare (due to the depleted worth of the money they hold), slaved to increase the national output by 2.54% and 3.46% in Tinubu’s first full 2 quarters in power.

Meanwhile, Nigeria’s national output, measured in dollars, moved down from the largest to the fourth in Africa, following the devalued Naira under Tinubu in 2023, according to data from the IMF.

These scenarios play out in a country where “Conflict and insecurity, rising inflation and the impact of the climate crisis continue to drive hunger” among 4 in 10 Nigerians living below the poverty line, according to the World Food Programme.

This data-driven report reviewed Tinubu’s policies, reforms, and economic plans and how these have affected the Nigerian economy in the last one year.

Economy: Unrelenting Productivity

There was an increase in real GDP and real GDP growth rate in the last three quarters of President Tinubu’s first year in office.

The real GDP growth between the 3rd and 4th quarter in 2023 could be as a result of these policies: fuel subsidy removal and the unification of the exchange rate.

The NBS records show that the GDP growth rate steadily grew from 2.51% in the 2nd quarter to 3.46% in the 4th quarter of 2023.

The real GDP increased from N17.94 trillion in the 2nd Quarter to N21.77 trillion in the 4th Quarter of 2023.

The annual real GDP (year on year) growth rate at the end of 2023 stood at 2.74%, while the annual real GDP growth (year on year) rate in 2022 stood at 3.10%. This is a 0.36% decrease from the total GDP in 2022.

The Real GDP reflects increases in consumer spending, exports, Federal, state, and local government spending, non-residential fixed investment, private inventory investment, and residential fixed investment.

In the last 25 years, most of the democratically elected presidents recorded successive quarterly real GDP growth in their first half year in office, including Tinubu.

The Buhari administration is the only democratic government in Nigeria where real GDP growth rate declined in the second quarter of his first half year, before the real GDP value decreased by 4.69% in his third quarter in office.

The growth in Tinubu’s time can be largely attributed to the rebound in the price of oil and the increase in the performance and activities in the service sector such as telecommunication, transportation, etc preceding the yuletide season.

The service industry grew by 3.98% in Q4 and contributed 56.55% to the aggregate GDP within that same period.

The recorded growth in the real GDP in the last three quarters of 2023 did not match the projected real GDP growth rate by the IMF and the World Bank for Nigeria. The projected real GDP growth rate was 3.3% for 2023.

While his policies supported an increased real GDP and real GDP growth rate, the other macroeconomic factors such as inflation and unemployment have worsened within a year.

The removal of the subsidy led to an increase in the price of petroleum by over 100%, and the unification of the exchange rate led to the devaluation of the naira by over 100%.

The shock from both policies led to the increase in the prices of transportation, food, services, foreign business transactions, etc. which has put a strain on the people’s purchasing power and aggregate consumer spending.

Economy: Unstable Prices

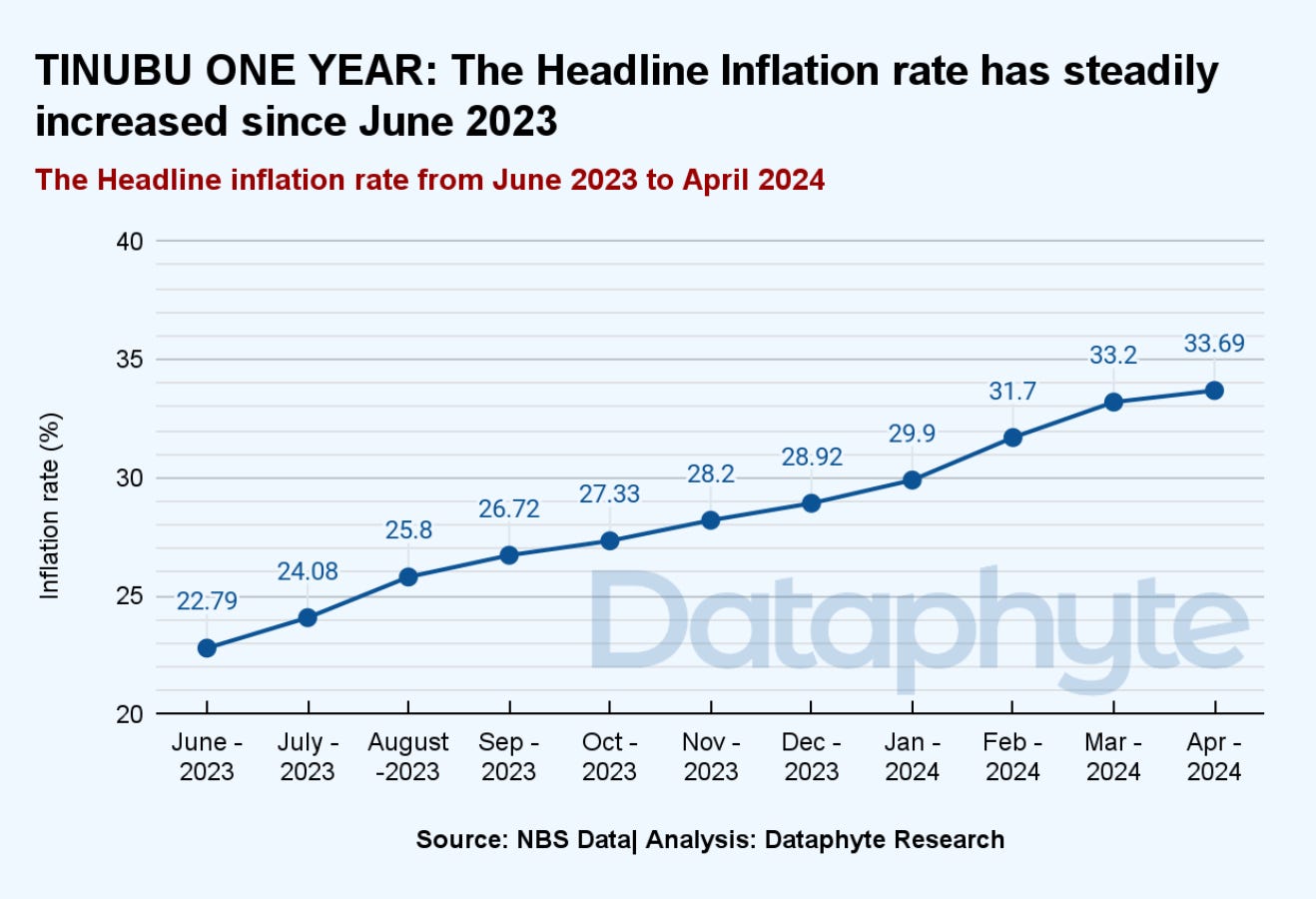

The headline, core, and food inflation rates are the highest they have ever been in the last 14 years.

The increase in inflation has been blamed on the policies and reforms put in place by Tinubu’s administration.

The headline inflation rate rose from 22.41% in June 2023 to 33.69% in April 2024. This is an 11.28% increase within Tinubu’s one year in office.

The average month-on-month inflation in Tinubu’s first year in office is 1.6%. This implies that prices of goods and services increased by an average of 1.6% within one year of Tinubu’s administration.

The food inflation rate in March 2024 stood at 40.01% on a year-on-year basis. This is a 14.76% increase from the food inflation in June 2023 which stood at 25.25%.

The core inflation rate which excludes the food and energy prices because of their volatility has also increased. The core inflation rate rose from 20.06% in June 2023 to 25.9% in March 2024 with a month-on-month increase of 2.54% growth rate.

The urban inflation rose from 24.38% in June 2023 to 35.18% in March 2024 with a month-on-month inflation growth rate of 3.17%.

The rural inflation rate rose from 21.37% in June 2023 to 31.45% in March 2024 with a month-on-month growth rate of 2.87%.

The inflation rate under Tinubu’s government is the highest in the last 25 years.

The lowest inflation rate of any Nigerian president's first year in office was under President Goodluck Johnathan’s government.

According to the NBS, one of the causes of the rising inflation rate is the currency devaluation.

The demand for foreign goods has increased. As the market becomes unpredictable due to the volatility in price of a Naira to a Dollar increases, the cost of the goods increases as well.

International prices

Within one year of Tinubu in office, the Naira had been devalued by about 42% between June 2023 and April 2024.

The Naira plummeted from N770.38 in June 2023 to N1330.21 in April 2024 against the dollar in 11 months, marking a N559.83 Naira surge.

The exchange rate surged higher under Tinubu’s government than any government between Yar'adua until now.

The Naira gained a value of N3.90 against the dollar during Yar'adua's one year in office compared to other governments.

The unification of the Naira reform made by President Tinubu is aimed at letting market forces determine the Naira’s value. It has resulted in a substantial devaluation of the country’s currency, with significant implications for the Nigerian economy.

According to the Governor of CBN, Mr Yemi Cardoso, the increase in the demand for imported goods led to the Naira devaluation and simultaneously to the decrease in the supply of US Dollars.

Employment: Unused Potentials

The unemployment rate increased by 0.8% between the 2nd and 3rd quarters of 2023.

It increased from 4.2% in the 2nd quarter of 2023 to 5% in the 3rd quarter of 2023.

The unemployment rate among youths shot up by 1.4% between Q2 and Q3. The rate was 7.2% in Q2 and 8.6% in Q3.

Urban unemployment increased from 5.9% in Q2 to 6% in Q3 while rural unemployment increased by a far greater margin of 1.5%; 2.5% in Q2 and 4% in Q3.

The number of workers actively participating in the labour force dropped from 80.4% in Q2 to 79.5% in Q3.

Nigeria has a high number of informal businesses. The number of self-employed workers is higher than salary earners.

Employment in the informal sector dropped from 92.7% in Q2 to 92.3% in Q3. The number of self-employed workers decreased from 88% in Q2 to 87.3% in Q3. The wage employment increased from 12% in Q2 to 12.7% in Q3.

The unemployment growth rate between Tinubu’s government and the previous governments cannot be fully ascertained as the measure for unemployment has changed since the 4th quarter of 2022.

Currently, NBS defines unemployment as only those not in employment, actively searching and available (did nothing for profit or pay).

If one works at least one hour within 7 days of a week, he/she is classified as employed, but underemployed.

Entanglement: Unfulfilled Promises

While the administration recorded real GDP growth, this represents only half of one of the 5 direct economic goals he set.

There is also the access to capital, particularly consumer credit. The government announced it has begun this lately, but measuring its adequacy and effectiveness, besides the transparency and inclusivity around it, maybe somewhat premature.

The remaining 3½ of the 5 direct economic goals set by Tinubu shows the President has not succeeded yet in these in his first year in office.

Food Security

Food Security tops the issues that the Tinubu administration vowed to prioritise, but food inflation rate, which measures changes in the prices of food in the market, shows that food affordability, a key component of food security, is fast becoming a daydream.

Sadly, the World Food Programme has predicted that 26.5 million Nigerians will suffer from acute hunger by June - August 2024 due to inflation, conflicts, and other climate conditions. This is a huge increase in comparison to the 18.6 million people who suffered from food insecurity at the end of 2023.

Food inflation rose from 25.25% in June 2023 to 40.53% in April 2024. This is a 15.28% increase in one year.

This food inflation growth is the highest recorded in the last 25 years.

Ease of Doing Business

One of the areas that was directly affected by the shock of the removal of fuel subsidy was transportation.

Transport costs impact trade, logistics and the ease of doing business within the country.

The announcement of the removal of fuel subsidy saw an increase of the price of petrol and petroleum products. Petrol prices increased from N165 to over N600 overnight last year.

According to the NBS report on transportation fares, on a year-on-year basis (March 2024 on March 2023) transportation costs increased across all forms of transport.

Bus journeys within the city increased by 49.55%, bus journeys interstate increased by 79.17%, airfare increased by 18.96%, motorcycle transport fares increased by 2.15%, and waterway transport fares increased by 34.25%.

Access to capital, particularly consumer credit

To curb the negative effects of the policies and reforms, the government intends that more Nigerians have access to consumer credits by introducing student loans and Federal government-assisted loans.

Furthermore, allocation from the Federation Account to the states, following the removal of the fuel subsidy, has increased significantly, releasing tremendous funds to the State Governments to reach the grassroots.

It is left to see how much these measures can untangle individuals and businesses from the financial entanglements the Tinubu policies have already lined them into.

Overall, in one year, Tinubu’s policy reforms has driven up the gross national product but visited economic hardship on the workforce that produced it.

In short, a depleted workforce, depleted wages, and depleted welfare is the simple way to describe the financial entanglements

In our assessment, Tinubu’s first year in the Presidency is marked by the people’s unrelenting productivity, precarious unstable prices, people’s unused potentials, and the president’s unfulfilled promises.

Of course, Mr Tinubu’s economic team has 2 more years to actualise his 8-point socio-economic agenda.

We wish them less of lip service and the best of luck!

And everyone, less of entanglements and the best of love!

Hope you enjoyed this edition of Data Dives. It was written by Lucy Okonkwo and edited by Oluseyi Olufemi.